Aerospace innovator Odys Aviation close Series A Funding to Accelerate Full-Scale Flight Testing and Global Operational Launches

Odys Aviation, a dual-use aviation company building hybrid-electric vertical…

AI business intelligence leader AlphaSense acquires Carousel to power AI-driven Excel modeling

AlphaSense News: AlphaSense Surpasses $500M in ARR as Adoption of Applied AI…

Reusable Rocket innovator Stoke Space Raises $510 Million to Scale Manufacturing of Fully Reusable Nova Launch Vehicle

Stoke Space News $510 Million Series D Funding and nears $2B valuation:…

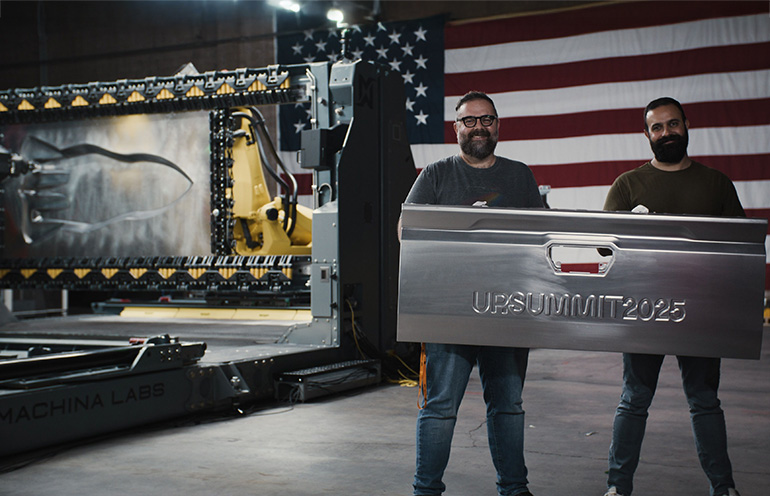

Toyota partners with Machina Labs to advance custom automotive manufacturing with AI and Robotics

ALSO READ: Robotics leader Machina Labs partners with U.S. Air Force to…

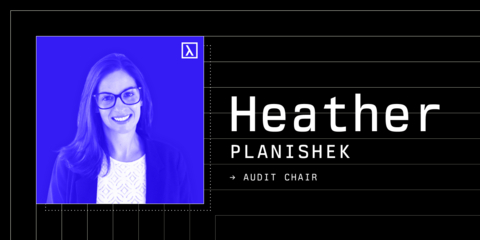

AI infrastructure leader Lambda appoints Heather Planishek to Board of Directors as Audit Chair

In preparing the Company for the public markets and IPO with Morgan Stanley,…

Robotics leader Machina Labs partners with U.S. Air Force to advance AI Driven manufacturing for defense

In partnership with the ARM Institute, this multiyear program will enhance the…

AI inference chip maker Groq raises $750 Million at $6.9 Billion as demand surges

ALSO READ: Groq more than doubles valuation to $6.9 billion as investors bet on…

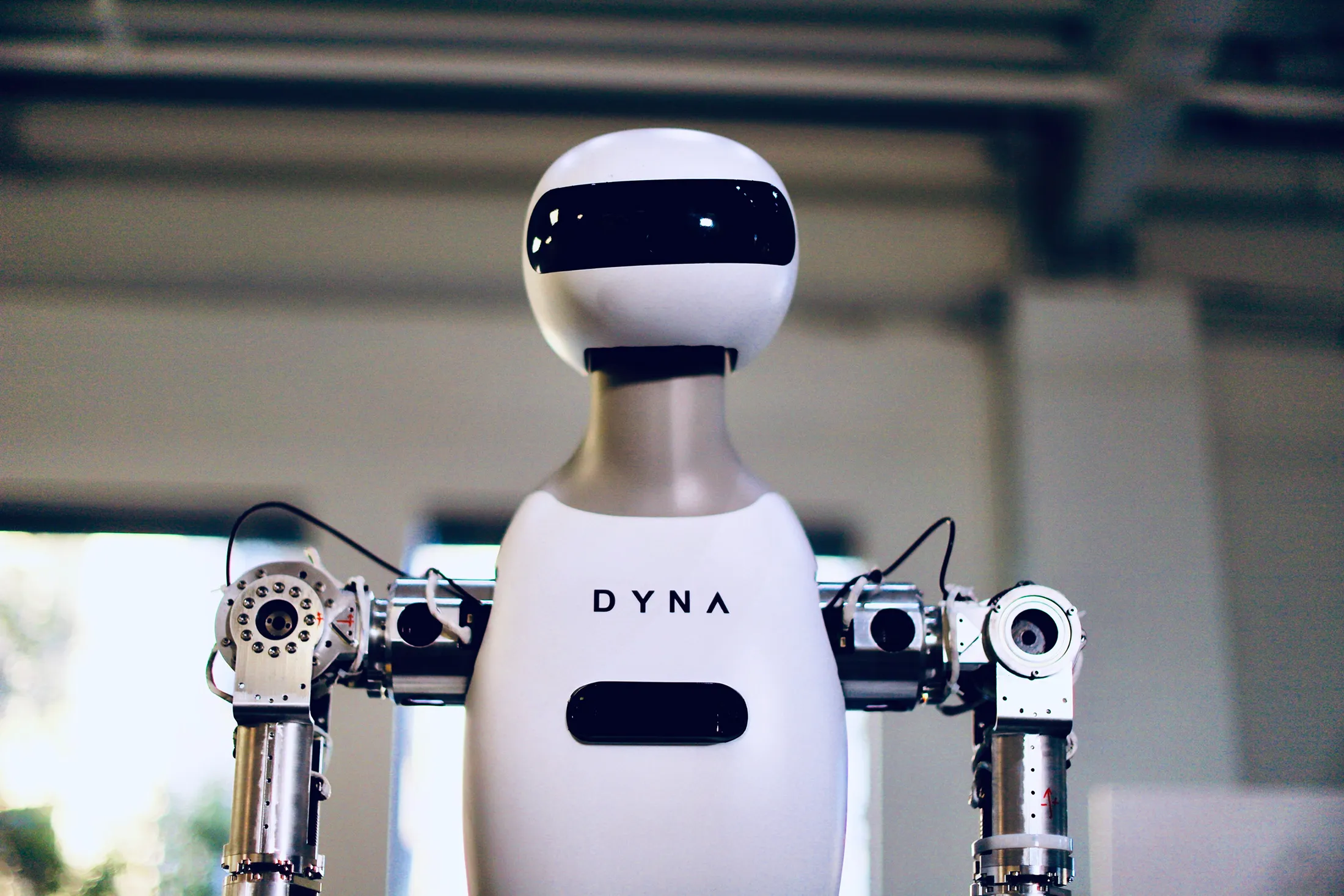

Dyna Robotics closes $120 million Series A to advance robotic foundation models on the path to physical artificial general intelligence

We are thrilled to participate in another piece of our disruptive robotics…

AI fintech innovator Kapital becomes LATAM's first $1.3 billion AI unicorn

What an incredible, disruptive AI fintech innovation journey since we invested…

Neurophos AI and Terakraft data center partner to pioneer the Future of Sustainable AI Computing

Neurophos is excited to announce its collaboration with Terakraft AS, a…